2023 will go down as one of the worst years in recent memory for the housing market.

It started with a continuation of negative trends from the end of 2022 and turned into the least affordable year for home buying on record. But even though high mortgage rates resulted in a severe drop in home sales, they also kept a lot of would-be sellers “locked in” to their low mortgage rates, and home prices continued to rise throughout the year as a result.

At the end of the year, activity slightly increased as positive inflation signals brought rates down. But will that continue as we move into 2024? And if it does, will more homebuyers enter the market? How will that increased demand impact home values?

To help with this analysis, we turned to Barry Habib and MBS Highway The data below is pulled from their 2024 Housing Forecast report.

Mortgage Rates

First things first, mortgage rates. While we expected mortgage borrowing costs to fall in 2023, they defied expectations and ended up reaching multi-decade highs.

Rates began the year 2023 on a downward slope, but quickly reversed course and surpassed 7% by spring. Things got even worse as rates climbed beyond 8% in October.

However, inflation has since cooled and economic reports continue to signal that the worst of it could be over.

The Federal Reserve has also gotten on board, and they are very optimistic about rate cuts in 2024. After raising rates 11 times in less than two years, there could be three or more cuts next year.

While the Fed doesn’t directly control mortgage rates, their monetary policy tends to correlate. As they cut rates in the face of a cooling economy, mortgage rates should also fall.

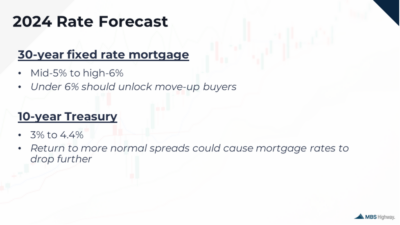

We anticipate 30-year fixed rates to decrease throughout the year, possibly reaching as low as the mid-5% range by December.

The way things are going, it could come sooner. And rates could go even lower, potentially dropping into the high-4% depending on loan product and qualification factors.

For current homeowners, this also means there will be more opportunities to refinance.

There were about $1.3 trillion in home purchase loan originations during 2023, despite it being a slow year. And rates have since come down quite a bit from what will likely be the highest point in this cycle.

Considering all those high-rate mortgages that funded over the past two years, we’re confident there will be a large pool of homeowners who will benefit from refinancing their current loans and see substantial savings on their monthly payments.

In addition, we might see homeowners tap equity via a cash out refinance if rates keep coming down and get closer to their existing rate.

Home Prices

Lately, there’s been a lot more optimism in the real estate market thanks to easing mortgage rates.

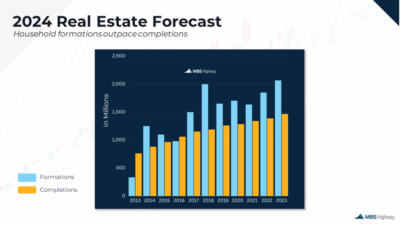

Housing inventory hit historic lows during the pandemic and a lack of supply has been a major constraint on the housing market. Supply has continued to remain low largely because of the “rate lock-in” effect.

Many homeowners who likely would have listed their homes for sale decided to stay put last year because of their ultra-low rates. Nationally, more than 60% of homeowners with a mortgage have an interest rate below 4%.

However, we believe supply will loosen up in 2024. Even homeowners who have been locked into low rates will increasingly find that changing family and financial circumstances will lead to more moves and more new listings over the course of the year, particularly as rates move closer to 6%.

More new listings will add to inventory, though overall supply will likely still remain low. This will continue to put upward pressure on home prices.

Between 2019 and 2022, the median home price nationally rose by more than 40%, or by about 13.7% annually, a much faster past of price appreciation than during a typical market. Strong demand during the pandemic, fueled by historically low mortgage rates and increased savings, drove up home prices.

Home price growth moderated in 2023, but still saw higher-than-average increases thanks to persistently low supply in the market. CoreLogic’s latest Home Price Insights report shows that prices were up 5.2% year-over-year in November 2023.

Looking ahead, several factors will push and pull home prices. More inventory will be generally offset by more buyers in the market. As a result, we believe home prices will rise at a similar pace they did in 2023 at an annual rate of 4.5-5%.

The Bottom Line

In 2024, we expect mortgage rates to drop closer to 6% in the wake of easing inflationary and less restrictive monetary policy.

These lower rates will bring more activity into the market. Demand will continue to overwhelm supply, and we believe we will see low-single-digit appreciation throughout the year.

We are confident that the housing market will remain steady in 2024 and beyond, and that real estate will continue to be a safe investment and a great way to build wealth.

If you would like to know if homeownership is a possibility for you this year, reach out to us today. We will be able to answer all your questions about the state of the housing market and help you put together a plan to get a great deal on a home and start building wealth through home equity when the time is right.