Understanding the “Housing Crisis” in the US vs China

Real estate in China has been unwinding over the last few years following a pattern similar to the U.S. in 2008 and 2009.

Lax lending standards, cheap credit, and a popular belief that real estate values never decline have created a massive bubble in the Chinese housing market, and the effects are just now starting to be felt.

When you see stories about the China housing collapse, you might think that the U.S. is experiencing a similar crisis. Although both real estate markets are struggling with their own challenges, these challenges could not be more opposing.

It’s important to understand the many differences between the U.S. and China housing markets, conflating the very different dynamics facing both markets would be a significant mistake.

China is Experiencing a 2008-Style Deflationary Housing Crisis

We know that China’s economy has experienced swift growth over the last few decades, accompanied by a housing market boom fueled by rapid population growth (from 667 million in 1960 to 1.43 billion in 2023, a 113.7% increase), upward economic movement by the Chinese middle class, and massive speculation in the residential real estate market.

China’s housing market is currently the biggest asset class in the world with an estimated value of nearly $60 trillion. About one third of China’s economic activity involves the real estate sector (compared to 15 to 18% of the American economy). These numbers are even more shocking when combined with the fact that housing accounts for about 70% of Chinese household wealth.

The current real estate crisis originated shortly after China relaxed its rules on private home sales back in 1998. This shift coincided with an already booming economy and resulted in millions of people moving from the country to the city for better economic opportunities. Real estate developers jumped at the opportunity to provide the homes this new group needed and could now afford.

The seemingly endless demand for housing put dollar signs in the eyes of Chinese investors looking for better returns, which made the supply problem even worse. Developers began to take on massive amounts of debt to keep up with the pace of demand and began selling properties in developments that hadn’t even begun construction (therefore shifting significant amounts of risk to the investor buyers).

The cracks started to show in the wake of the COVID-19 lockdowns. The slower pace of home sales meant less cash flow for the highly leveraged developers who began to default on their credit lines, and construction stopped on many of the unfinished projects that had already been sold to buyers who had taken out mortgages to buy those unfinished units.

Many of these borrowers were left paying a monthly mortgage on nonexistent homes. In the summer of 2022, these frustrated borrowers refused to make payments and called for a nationwide mortgage boycott.

Since then, the Chinese government has intervened to ensure that property developers have sufficient credit to deliver on unfinished homes and that potential home buyers are incentivized with attractive mortgage rates and better financing terms.

Key Differences Between U.S. and China Housing Markets

Population Growth & Housing Completions

After more than doubling from 1960 to 2023, China’s population is now the fasting aging population in the world, and new household formations have been declining since 2013 alongside the falling marriage and birth rates.

Between 2010 and 2020, demand for residential properties in urban China averaged 18 million units a year. As China’s population ages and demand for replacement properties fall, Goldman Sachs estimates that number will drop to 6 million units a year by 2050.

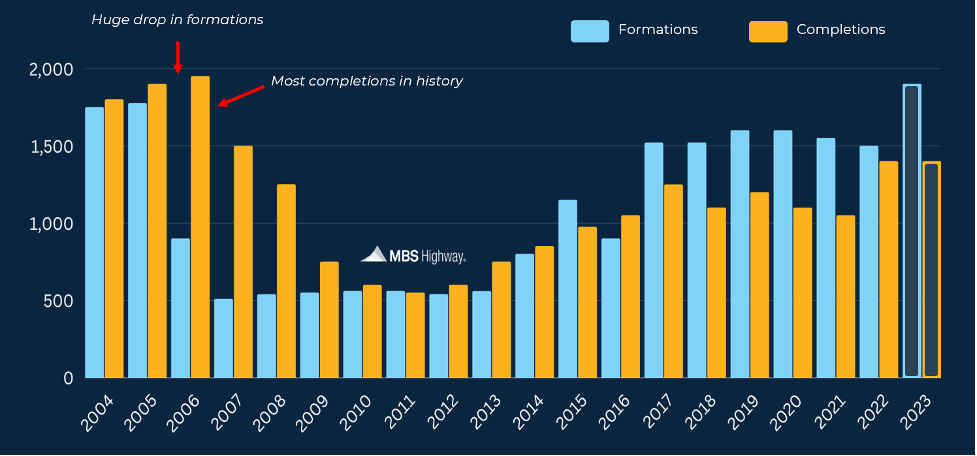

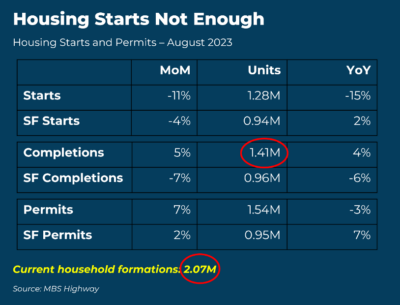

While China is experiencing the fallout from years of overbuilding, the United States is experiencing the opposite. In the years following the Great Recession, builders massively pulled back on residential construction. We still have not recovered from that period, and new households have been significantly outpacing new home completions since 2015.

Since 2015 household formations have significantly exceeded household formations and this trend continues to this day, where we see an estimated 600k deficit in the number of residential completions needed to match household formations.

Interest Rates on Mortgaged Homes

China’s mortgage market also differs significantly from the U.S. in that almost all of China’s $5.6 trillion in residential mortgages are adjustable-rate mortgages. The effective interest rate on these mortgages resets once a year.

While the country has taken steps to lower interest rates on new and outstanding mortgages, adjustable-rate loans make the dangers of mortgage default much more prevalent. This was a big factor in the US foreclosure crisis leading up to the Great Recession. Foreclosed homes add to market supply and can cause home prices to decline when rates continue to rise and demand wanes.

Things are different in the U.S. where nearly 90% of all mortgages have a fixed rate and most of these fixed rates are lower than current market rates. Nearly two-thirds of all mortgages out there today have an interest rate below 4%, and nearly a quarter have a mortgage rate below 3%. Most of these homeowners will not budge and will continue to enjoy their low, fixed-rate mortgage for many years to come.

Credit Availability

Leading up to the housing market crash, subprime mortgage loans were the norm, and qualifying for a home (and multiple investment properties) was easy to do. This resulted in a buying spree from people who could not pay their mortgage payments.

Lending standards have tightened drastically since then, which you can see represented in the Mortgage Credit Availability Index. The higher the index, the easier it is to obtain a mortgage loan. The index hit an all-time high in 2007, and in the fourteen years since the credit bubble deflated in 2008 it has become much more difficult for mortgage applicants to obtain credit approval.

To encourage more buyer demand, China has made it easier to qualify for a mortgage. Guangzhou, China’s fifth biggest city, announced in August that mortgage curbs would be eased, allowing home buyers to enjoy preferential loans for first-home purchases regardless of their previous credit record.

When it’s easier to qualify for a mortgage, it’s more likely that people will default on that debt. To increase homebuyer demand by lowering mortgage standards, China may be setting itself up for an even larger crisis in the future if those adjustable-rate loans cannot be paid back.

Amount of Vacant Homes

He Keng, the former deputy director of China’s National Bureau of Statistics, said at the 2023 China Real Economy Development Conference that there is an oversupply of properties in Chinese cities that even China’s 1.4 billion people may not be able to fill.

Qiu Baoxing, former vice-minister of Housing and Urban-Rural Development, had also said at the Chinese Cities Urban and High-Quality Development Forum in 2022 that the housing vacancy rate has reached 15%, with some provinces even hitting the 25% to 30% mark.

Even in the face of reduced buyer demand, a lack of available housing inventory has helped keep housing costs high throughout most of the United States.

According to the Census Bureau, national vacancy rates in the third quarter of 2023 were 6.6 percent for rental housing and 0.8 percent for homeowner housing. Homeowner vacancy rates in the US are the lowest they’ve been ever.

The Chinese real estate market is nothing like the U.S. market. We’ve experienced a shortage of new construction for nearly a decade, improving demographics of buyers (Millennials, Gen X, and Gen Z), very tight lending standards, historically low fixed-rate mortgages, and the tightest real estate inventory and vacancy rates ever in history.

For those seeking further insights into the mortgage industry and how these global economic trends might impact the local housing market, reach out to us. We’re here to provide comprehensive information and guidance tailored to your specific inquiries. Contact us to dive deeper into the complexities of the real estate landscape and its potential influences on the mortgage sector.